Volatility in the stock market has begun to pick up this quarter from a very low base. We want

to talk about some of the things that have investors nervous right now.

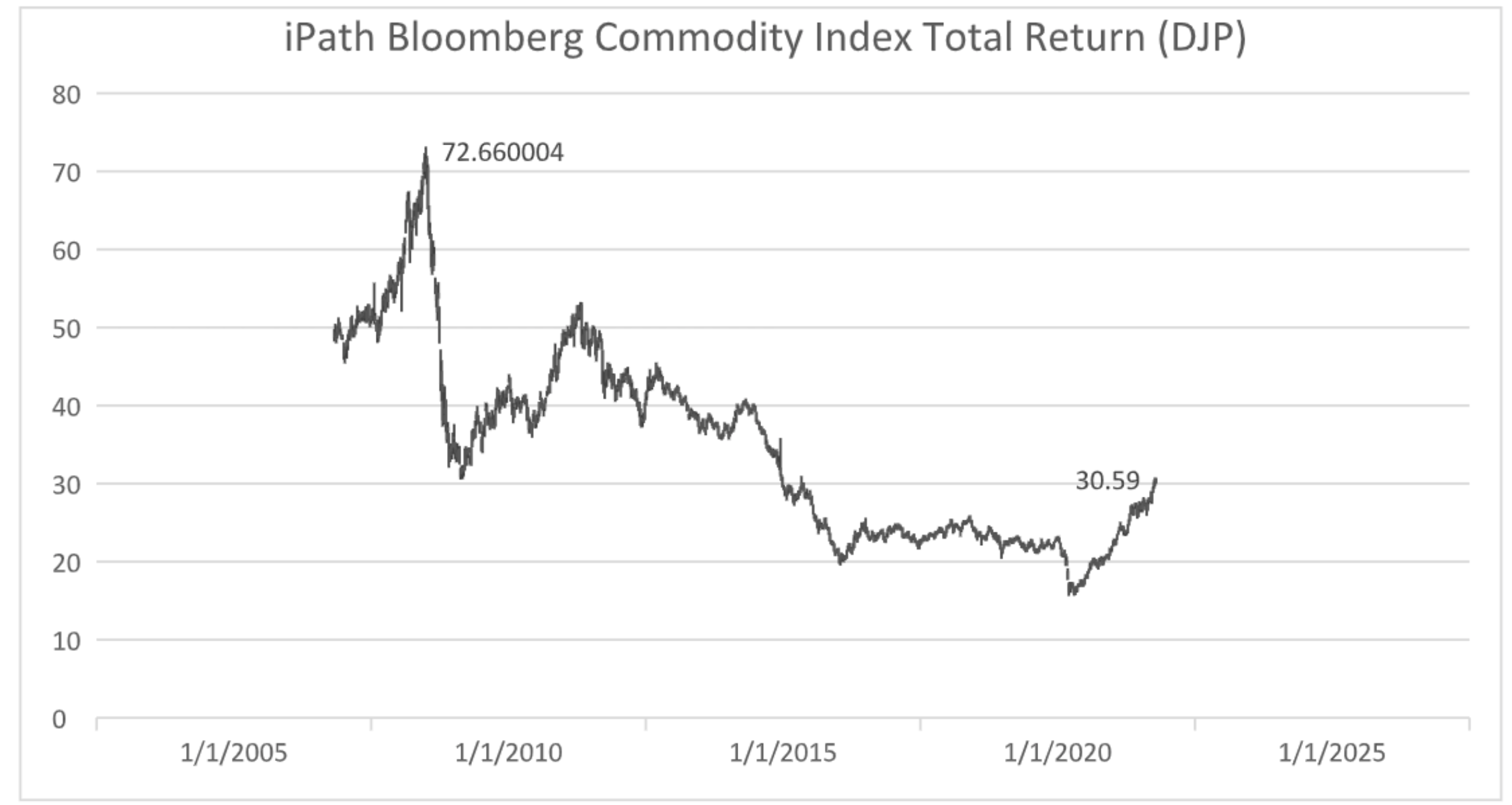

We have been predicting for the last few years that we are headed for much higher energy and

commodity prices. The chart below represents what a basket of commodities has done since

2007.

As you can see, commodities as a group are at five-year highs. You can also see that they are

still down over 50% from their 2008 highs. Are we going to challenge the old highs? We think

there is a chance we might. Let us elaborate.

Oil and all its derivatives represent about 33% of this index. Oil prices have been in a bear

market for about seven years now. We think that trend has ended, and prices are headed

higher. Why? In 2013 when a barrel of oil was over $100, we had over 1,900 rigs drilling for oil

in the United States. When oil was close to $150 a barrel in 2008, we had over 2,000 rigs drilling

for oil. Today we are at 500 rigs drilling, which is up from the low of 250 last year. We are at

very depressed levels for oil drilling.

In 2011 the U.S. produced only 5 million barrels of oil a day. At its peak in 2020 we produced

13.2 million barrels a day. Today we are producing about 11 million barrels a day. Almost all the

gains in U.S. production came from fracking. We have written in the past that we think fracking

for oil is a poor business model. Fifty percent of the oil produced from a fracked well is in year

one and then it declines dramatically. You are constantly having to drill more and more wells to

stay even in oil production. You are NOT finding large pools of oil with fracking. You are taking marginal wells

and trying to “squeeze” a few more drops of oil out of it before you move on to the next well.

The world consumes about 100 million barrels of oil a day. It is projected that the world will

need around 120 million barrels of oil produced a day to satisfy world demand in the next 20

years. Very few (not us) saw oil production in the U.S. growing by 8 million barrels over the last

10 years to cause an oil glut in the world markets. The U.S. has been the only area of the world

that has grown production by any meaningful amount over the last decade.

The environmental, social and governance movement (ESG) has targeted oil companies as evil.

They were able to get seats on the Exxon board while only owning 1% of the stock. The Exxon

board then announced they were reducing the amount of money they spend on oil and gas

exploration. The ESG movement has helped restricted the flow of capital to any energy

producing company that isn’t in the wind or solar business. This is going to cause a real problem

soon in the energy markets.

Wind and solar (ESG favorites), according to the Energy Information Administration (eia.gov),

produced 3% of the energy consumed in the United States as of 2019. Oil and natural gas

represent 69%. By restricting capital to the oil and gas business, we are taking a huge leap of

faith that we won’t have oil and gas shortages soon. The ESG movement is assuming we can

replace that lost production with wind and solar. We see no way that happens over the next 5

or even 10 years. What is concerning to us is the next two years. As the world economy

recovers from covid, we don’t think there is going to be enough oil to go around. The record

lows in oil rigs drilling will start to show up in less production in the U.S. It is our guess that once

oil produced in the U.S. goes below 9 million barrels a day, oil will be at least $100 a barrel. We

are not sure how our politicians are going to react to this. Will they tell you to turn down your

thermostats this winter to ease the crunch? Will they tell the environmentalists to have some

patience with moving from 3% wind and solar production to 10% over the next 10 years? Will

they blame the oil companies for restricting drilling and causing a shortage? Will the EPA ease

up on methane restrictions and clean-air zones? Will the government make it easier to build

solar and wind farms by easing the restrictions on government permitting (stop not in my

backyard protests)? We don’t know the answers to these questions today but we are going to

find out soon.

Eighteen months ago we had around 900 rigs drilling for oil, which in our opinion was not going

to keep us at 13 million barrels a day produced in the United States. With the rig count

averaging 400 rigs drilling for the last 12 months, time is ticking for a potential energy shortage

to occur. Please remember that around 50% of a fracked well’s production occurs in year one.

The shortages should start to show up in Q4 of this year due to a lack of new rigs looking for oil.

So what do you do about this? We own oil stocks, gold stocks, Latin American stocks, real estate

stocks and oil trading companies, to name a few. To hedge our bets, we continue to have a very large position

in Tesla. Electric cars are the way of the future as is power storage and solar

panels. Tesla should do well in that environment. Electric cars won’t be able to move the needle

quick enough to change the supply demand imbalance we see coming. Relatives and employees

of Trend Management own five Teslas. We love the product but it’s not going to help us out of

this mess soon.

If we are right on our oil prediction it will cause our balance of payments in world trade to get

worse for the U.S. This will cause the dollar to go lower, which will cause other commodities to

go higher (wheat, corn etc). It will be a negative feedback loop that will be hard to stop in the

short-term.

When oil prices rallied in 2000 it marked the end of the dot-com bubble. During that time

frame, value stocks did very well and dot-com stocks dropped over 50%. We owned value

stocks then and we do now. We think something similar could happen in 2021-22 though not to

the extremes like 2000. Higher inflation and commodities will “suck” money out of the QQQ

index and push it into value. Will it be the same? Nope. Will it look familiar? Yes, we think so.

This letter may seem a little depressing talking about oil shortages and rising prices. It may

never happen. It’s our job to invest based on what we believe is going to happen for a company

as well as on a macro basis. So far this year oil prices are up over 50% and we are having a good

year. We think that can continue. We think, for growth stocks, this market is going to be much

more difficult based on what we wrote above.

We think the world has become overly complacent about inflation. The next 18 months will test

that complacency. We haven’t bought a government bond for clients in over 13 years. Maybe

we do that at the end of this cycle. We are predicting a problem and we have invested

accordingly. We hope we are right. Feel free to call us at 417-882-5746 to discuss it.

Our holiday party is back on this year. We will have it at Highland Springs from 6 to 8 on

December 23 rd . You will receive and invite in the mail after Thanksgiving. We look forward to

seeing everyone in person again.

Sincerely,

Mark Brueggemann IAR Kelly Smith IAR Brandon Robinson IAR